Investing In Your Future

Investing In Your Future

5 Financial Lessons Everyone Should Learn

Welcome to Soulful Sunday #12 for April 2, 2023.

If you’re new to The Power of Change, welcome, and thanks for spending a few minutes of your day with me.

What’s new this week:

I. Investing In Your Future: 5 Financial Lessons Everyone Should Learn

II. Master Your Monday - A mindful tip to help you start the week.

III. Vision For You - An idea or image to help you create a vision of your life.

Investing In Your Future

5 Financial Lessons Everyone Should Learn

There’s been much debate recently about the financial moves of the Federal Reserve in the US. Are the attempts to slow inflation working or worsening the problem? Many Americans struggle to make ends meet as inflation erodes purchasing power. The rapid increase in home and rental prices since the pandemic has created a housing affordability crisis, leaving many prospective homebuyers on the sidelines.

As a real estate agent, I work with people who make large financial decisions every day. Whether clients are first-time homebuyers or seasoned investors, economic forces affect decisions.

While there are no easy answers when it comes to the economy, financial planning is one way to help ease the ups and downs that are inevitable with changing economic times.

The earlier you understand the concepts of financial literacy, the better.

When I began homeschooling my son, I incorporated many life lessons into his daily learning, including the principles of financial literacy and the importance of saving, investing, and preparing for financial emergencies.

When he was nine years old, I began teaching him about the stock market. Since then I’ve added to his understanding of investing and taught him the many principles of financial literacy I wish I had learned at his age.

5 financial lessons everyone should learn

Save early to take advantage of compounding interest

Many parents start saving early for education expenses for their children, and they’re wise to do so. By utilizing the concept of compounding interest, the money invested grows significantly over time.

It’s why this was the first lesson I taught my son.

Whether you’re saving for retirement, your child’s education, or your first home, understanding the power of compounding interest helps provide the incentive you need to save.

When your children are old enough to understand how money grows, explain it and show them on paper.

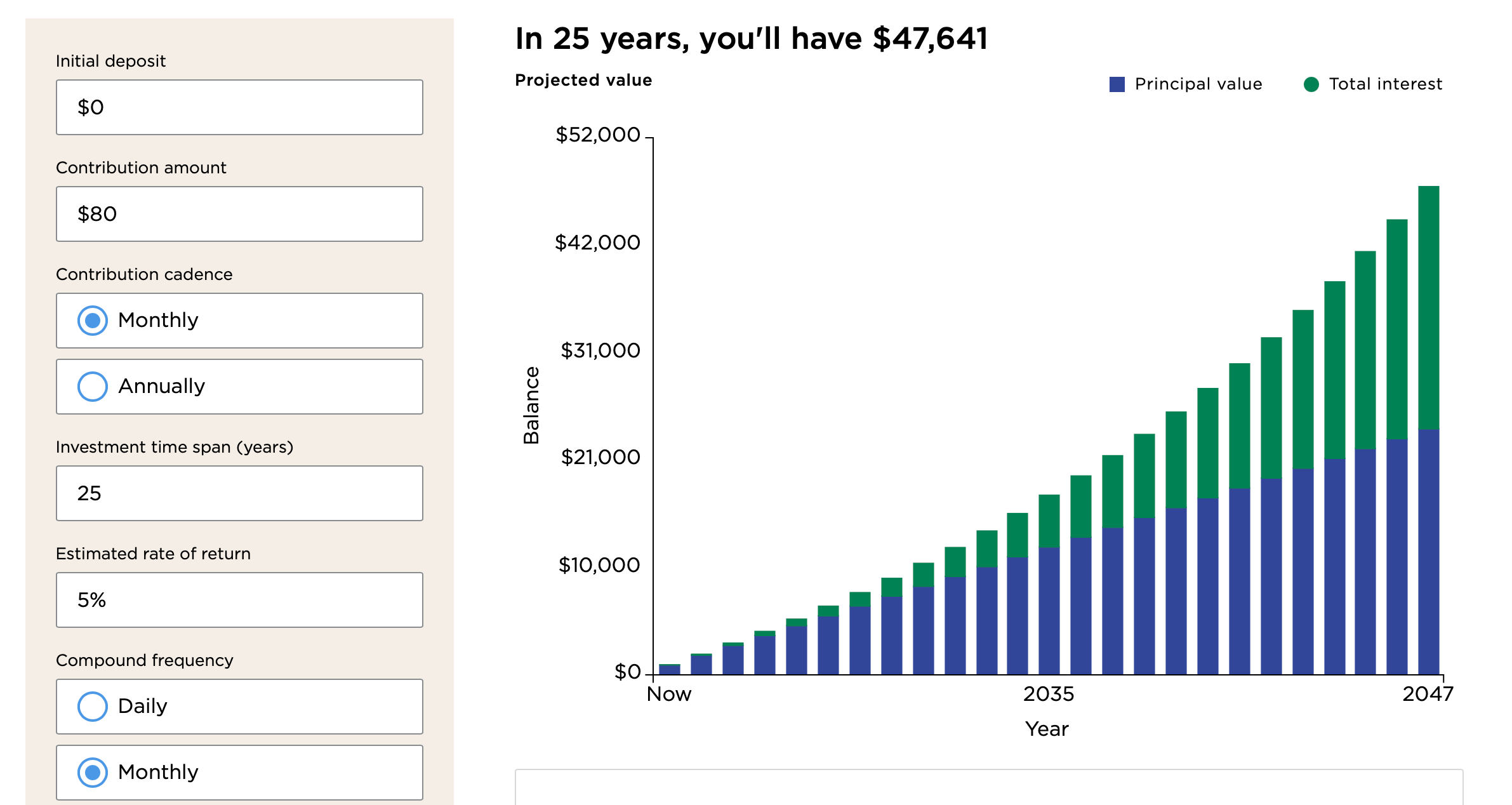

Below is a chart that shows what happens when you save as little as $20.00 a week in an investment account that earns an average of 5%.

If you began saving when your child is born, when they’re 18, the money would have grown to nearly $30,000, and in 25 years, to nearly $50,000

If you never contributed more than 20.00 a week for 50 years, you’ll have saved more than 213,000.00.

It wasn’t until I was studying business in college that I fully understood the power of compounding interest. If I had learned this as a teenager, I could have saved considerably more money before I became ill at 26.

Pay yourself first

Some may suggest that the cost of living is such that saving even 20.00 a week is difficult. I understand that as well as anyone. Medical expenses have dramatically reduced my ability to save for more than two decades, but I never stopped saving what I could. The best way to save is to pay yourself first.

I taught my son this by using an allowance as an example. I explained the importance of saving 20% of what you earn to invest in your future.

I explained if he received $5.00 a week in an allowance, he needed to save at least $1.00 or 20% of what he earned. Then I reminded him of the power of compounding interest in the first example.

Have an emergency fund

If you teach your children to save 20% of their earnings, teach them about an emergency fund too. Taking the example of the $5.00 allowance, have them set aside $1.00 in an emergency fund.

While it may be difficult for most children to understand the need for an emergency fund, it wasn’t hard for my son because his life changed dramatically at 11 when he suddenly became ill. The carefree days of school, baseball, and spending time with friends quickly turned into a life filled with doctors, medical treatments, and an uncertain future. His life changed in every way possible.

The first summer he was ill, we canceled the plans for our summer vacation. He was too sick to go, but by the third year, when we really could have used a vacation, medical expenses had become significant. It was hard to explain to my son that I didn’t have the money to do certain things, but it was the reality, so I used it as a teaching opportunity.

Medical bills made it necessary for me to prioritize financial decisions, and I shared this lesson with him. I explained that even though we had the best health insurance available, it didn’t cover all of our expenses and that’s why it’s important to have an emergency fund.

The truth was that the best health insurance plan covered less than 20%.

What most people don’t know is that 66% of people who file for bankruptcy cite medical issues as the reason for their financial downfall. Most have health insurance, but health insurance doesn’t protect you like you think it will.

Emergencies happen every day.

I know several families that have been forced to file for bankruptcy or lost their homes due to medical expenses.

Avoid debt that doesn’t grow your income.

A car payment is a debt that offers you little other than transportation. As soon as you drive it off the lot, it loses 9-11% of its value. I drive a car that’s ten years old. It runs great and doesn’t look its age. I could buy a newer car, but it’s not a priority, and I like not having a car payment. When my car begins to cost me more than it offers, I’ll look to replace it with a gently used model.

Invest in assets that pay you, such as real estate and dividend-paying stocks.

Taking out a loan to purchase real estate - whether your primary home or investment property is different from a car payment- it builds equity. Equity is the value of your home minus what you owe. The larger the down payment, the more equity you have. If you can’t make a large downpayment but are able to reduce the mortgage over time by making additional mortgage payments, your equity grows faster.

Investment property is real estate you purchase to generate income by renting it. It’s often considered ‘passive income’ because you’re not working to generate that income as you do in your primary job. Instead, the rent generated is more than the debt you took on to purchase the property and the expenses to maintain it. The rent reduces the debt over time, and if you hold the property long-term, you’ll have an asset that is free from debt and worth more than when you purchased it.

Scroll Facebook or YouTube, and you’ll see ads touting the success of short-term rentals, house flipping, or house hacking. Learning to invest in real estate requires education. I didn’t learn at a young age, so I’m teaching my son what I wish I had known when I was 17.

Investing in dividend-paying stocks is another great way to realize gains from the money invested in stocks. In addition to owning stock in a company, many companies pay dividends on your shares, increasing your overall return.

Whether saving for retirement, or to send your children to college, investing in your future doesn’t have to be hard. If everyone taught their children financial literacy, more adults would be in a better financial position.

II. Master Your Monday - A mindful tip to help you start the week.

Do not save what is left after spending, but spend what is left after saving.

– Warren Buffett

III. Vision For You - An idea or image to help you create a vision of your life.

If you’re saving to purchase a home or to take a vacation, make a vision board that helps you stay on track with your goals. Since I haven’t been on vacation in many years, I’m looking forward to the day I’ll be sitting in one of these lounge chairs. In the meantime, I’m saving as much as possible for my future andmy son’s.

Why Soulful Sunday?

I began The Power of Change to explore the potential to transform your life in meaningful ways.

Being mindful of your life is the first step.

Being mindful helps you focus on what’s important today and throughout the week.

If you enjoyed this edition, share it with a friend who may find it helpful.

If you’re considering buying or selling real estate, regardless of location, I’d love to help! I have an extensive referral network and work with agents all over the country. Reach out by email to learn more.

Interested in learning more about a topic I’ve discussed recently? I’d love to hear from you!

Great Info